Pennsylvania Estate & Property Tax Expertise | Certified Probate Real Estate Specialist

Confused About Pennsylvania Estate Property Taxes?

Navigating Pennsylvania Inheritance, Property & Estate Tax Obligations

Pennsylvania has some of the most complex—and expensive—estate and property tax requirements in the nation. Between inheritance tax (due within 9 months), ongoing property taxes, potential federal estate tax, and income tax implications, executors face a maze of obligations with serious financial consequences for mistakes.

As Pennsylvania's Certified Probate Real Estate Specialist (CPRES), Joe Thomas helps executors understand and navigate all property-related tax obligations throughout Montgomery, Philadelphia, Bucks, Delaware, and Chester counties. We provide clear guidance, strategic planning, and connections to tax professionals who ensure compliance while minimizing estate tax burdens.

Four Types of Taxes Affecting Pennsylvania Estate Property

Executors must navigate multiple tax obligations simultaneously. Here's what you need to understand:

Pennsylvania Inheritance Tax

What It Is:

State tax on the transfer of assets from deceased to beneficiaries. Based on relationship to deceased, NOT estate size.

Tax Rates:

0% - Spouse to spouse

4.5% - Direct descendants (children, grandchildren, parents)

12% - Siblings

15% - All other heirs (nieces, nephews, friends, etc.)

0% - Charities

Key Deadline:

9 months from death (full payment due)

3 months for 5% discount (significant savings)

Applies To:

Real estate in Pennsylvania

Bank accounts

Investment accounts

Personal property

Business interests

Everything the deceased owned

Who Pays:

Technically the beneficiary receiving property, but executor responsible for filing and payment from estate funds.

Property Taxes

What It Is:

Annual real estate taxes owed to county, township, school district. Continues regardless of death or probate status.

Why It Matters:

Deceased may have been behind on payments

Taxes continue accruing during probate (9-18 months)

Delinquent taxes create liens preventing sale

Sheriff's sales can force property liquidation

High priority debt (paid before most creditors)

Pennsylvania Rates:

Among highest in nation - typically

2-3.5% of assessed value annually

Montgomery County:

Highest rates in region

Philadelphia:

Tax abatement programs available

Bucks/Delaware/Chester:

Varies by township

Executor Responsibility:

Must pay current and delinquent property taxes from estate funds before distributions to beneficiaries.

US Federal Estate Tax

What It Is:

Federal tax on the total value of estates exceeding exemption threshold. Separate from inheritance tax.

2025 Exemption: $13.99 million

per person

$27.98 million

for married couples (with portability)

Tax Rate: 40%

on amounts exceeding exemption

Reality for Most:

Only about 0.1% of estates owe federal estate tax. If estate is under $14 million, you don't worry about this.

If Applicable:

Due 9 months from death

Requires filing Form 706

Complex valuations required

Estate planning attorney + CPA essential

Income Taxes

What It Is:

Regular income taxes on earnings during the year of death and during estate administration.

Types:

Decedent's Final Income Tax (Jan 1 - date of death)

Estate Income Tax (income earned by estate during administration)

Capital Gains Tax (if estate sells appreciated assets)

Key Points:

Rental income during probate = estate income

Interest/dividends on estate accounts = estate income

Sale of appreciated property may trigger capital gains

Estate gets new tax ID number (EIN)

Separate tax returns for estate

Due Dates:

Final individual return: April 15 following year of death

Estate returns: Quarterly estimated payments if applicable

Who Handles:

Typically estate CPA or tax preparer, coordinated by executor.

The Complexity Problem:

Most executors must deal with ALL FOUR tax types simultaneously, each with different deadlines, calculation methods, and filing requirements. Missing deadlines or making calculation errors can cost the estate thousands in penalties, interest, and lost discount opportunities.

That's exactly why PA Probate Help exists -

to guide you through these overlapping obligations and connect you with tax professionals who specialize in Pennsylvania estates.

Pennsylvania Inheritance Tax: What Executors Must Know

Pennsylvania inheritance tax is often the largest single tax obligation facing estates. Unlike federal estate tax (which most don't pay), virtually every Pennsylvania estate owes inheritance tax. Understanding how it works, when it's due, and how to minimize it can save tens of thousands of dollars.

How Pennsylvania Inheritance Tax Works

The Fundamental Concept: Pennsylvania taxes the privilege of receiving property from a deceased person, not the estate itself. The tax is based on:

Who receives the property (relationship to deceased)

What they receive (type and value of property)

NOT based on estate size -

even small estates pay inheritance tax

if property transfers to taxable beneficiaries.

Tax Rates by Beneficiary Relationship

According to Pennsylvania law (20 Pa.C.S. § 2111-2117):

Relationship to Deceased

Spouse

Parent (from child ≤21)

Lineal Descendants

Siblings (brothers, sisters)

Other Heirs

Charities

Tax Rate

0%

0%

4.5%

12%

15%

0%

Example on $100,000

$0

$0

$4,500

$12,000

$15,000

$0

Important Note:

Parent-to-child inheritance at 4.5% is most common scenario. If deceased left everything to 3 adult children equally, each child's inheritance is taxed at 4.5%.

What Property Is Subject to Inheritance Tax?

Pennsylvania inheritance tax applies to:

Real estate located in Pennsylvania

Tangible personal property in Pennsylvania (cars, furniture, jewelry, etc.)

Bank accounts (regardless of location if deceased was PA resident)

Investment accounts (stocks, bonds, mutual funds)

Business interests

Retirement accounts (IRAs, 401(k)s - with some exemptions)

Life insurance (if payable to estate rather than named beneficiary)

Annuities

Debts owed to deceased

Special Rules:

Joint Bank Accounts:

Taxed on deceased's "contribution" (often presumed 50% unless proven otherwise)

Jointly with spouse = 0% tax

Jointly with child = 4.5% tax on deceased's half

Jointly Owned Real Estate:

With spouse + right of survivorship = 0% tax

With others = percentage based on ownership and contribution

Property Transferred Within 1 Year of Death:

"Contemplation of death transfers" may be subject to tax if made to avoid inheritance tax.

Property Tax Exemptions and Exclusions

Family Farm or Business Exemption:

Qualifying family-owned businesses and farms transferred to family members may be 100% exempt from PA inheritance tax (effective July 1, 2013).

Requirements:

Business/farm owned by deceased for 5+ years before death

Transferred to qualifying family member (child, sibling, etc.)

Complex qualification criteria - requires attorney guidance

Family Exemption:

First $3,500 of tangible personal property to spouse or children is exempt.

Life Insurance:

Proceeds paid to named beneficiary (not estate) = exempt from inheritance tax

Critical Deadlines and the 5% Discount

Full Payment Deadline:

9 Months from Death All Pennsylvania inheritance tax must be paid within 9 months or become delinquent, triggering:

Interest charges (currently ~6% annually)

Penalties for late payment

Collection actions by PA Department of Revenue

Early Payment Discount:

3 Months from Death Pennsylvania offers 5% discount on inheritance taxes paid (not just filed) within 3 months of death.

Example Savings:

Estate value to children: $500,000

Tax at 4.5%: $22,500

Pay within 3 months discount (5%): $1,125 savings

Pay within 3 months = $21,375 total tax

Strategic Consideration:

Executors often estimate tax, pay early to capture discount, then file formal return by 9-month deadline with final calculations. If you overpaid, you get refund with the discount applied. If you underpaid, you pay balance but still got discount on the prepayment.

Why Property Sales Matter:

Selling estate property quickly (within 3 months) provides cash to capture this significant discount. On large estates, the 5% discount can save $5,000-$25,000+.

How to Calculate Pennsylvania Inheritance Tax

Step 1:

Value Everything

Determine fair market value of ALL estate assets as of date of death:

- Real estate (professional appraisal recommended)

- Bank accounts (balances on date of death)

- Investment accounts (market value on date of death)

- Personal property (appraisal for valuable items)

- Business interests (professional valuation)

- Vehicles (NADA/KBB value)

Step 2:

Subtract Allowable Deductions

Funeral expenses (up to reasonable amount)

Debts owed by deceased (credit cards, personal loans, medical bills)

Mortgages and liens on property

Estate administration costs (attorney fees, executor compensation, probate costs)

Federal estate tax (if applicable - rare)

Step 3:

Allocate Net Estate to Beneficiaries

Determine what each beneficiary receives under the will (or intestacy law).

Step 4:

Apply Tax Rate

Apply tax rate based on each beneficiary's relationship to deceased:

- Child receives $100,000 → $100,000 × 4.5% = $4,500 tax

- Sibling receives $50,000 → $50,000 × 12% = $6,000 tax

- Friend receives $25,000 → $25,000 × 15% = $3,750 tax

Total Tax Owed:

Sum of all individual beneficiary taxes

Real Estate and Inheritance Tax

Property Creates Unique Challenges:

Valuation Issues:

- Must determine fair market value at date of death

- Professional appraisal recommended (required for large estates)

- Disputed valuations can be appealed

Liquidity Problem:

- Tax is calculated on property value

- But property doesn't provide cash to pay the tax

- Estate must have cash from other sources OR sell property

Property Sales and Tax Planning:

- Selling property within 3 months allows capturing 5% discount

- Property sale proceeds can pay all estate taxes

- Strategic timing critical

Property Distributed vs. Sold:

If property distributed to heir "in kind" (they receive the property itself), they're responsible for their share of inheritance tax

If property sold by estate, tax paid from proceeds before distribution

Filing Requirements

Who Files:

Executor or administrator files Pennsylvania Inheritance Tax Return (Form REV-1500) with county Register of Wills.

What's Filed:

- Complete asset inventory

- Asset valuations

- Beneficiary information

- Deductions claimed

- Tax calculation

- Payment (check or money order)

Where to File:

- Montgomery County → Norristown

- Philadelphia County → Philadelphia

- Bucks County → Doylestown

- Delaware County → Media

- Chester County → West Chester

Payment Made To:

"Register of Wills, Agent" (Register acts as collection agent for PA Department of Revenue)

Extensions:

One 6-month extension available (file Request for Extension form), but:

- Must be requested before 9-month deadline

- Extension for filing, NOT payment

- Interest charges continue on unpaid amounts

- No extension for the 3-month discount window

Common Mistakes and How to Avoid Them

Mistake #1:

Missing the 3-Month Discount

Cost:

5% of total tax (often $1,000-$10,000+)

Solution:

Estimate tax early, make prepayment within 3 months even if unsure of exact amount

Mistake #2:

Incorrect Valuations

Problem:

PA Dept of Revenue can challenge valuations and assess additional tax + interest + penalties

Solution:

Professional appraisals for real estate and valuable personal property

Mistake #3:

Forgetting Joint Account Rules

Problem:

Assuming joint accounts avoid inheritance tax (they don't in PA)

Solution:

Understand PA's contribution test for joint property taxation

Mistake #4:

Not Claiming All Deductions

Problem:

Paying more tax than necessary

Solution:

Work with estate CPA to identify all allowable deductions (funeral, debts, admin costs)

Mistake #5:

Distributing Assets Before Tax Paid

Problem:

Personal liability for executor + beneficiaries still owe their taxes

Solution:

Pay all inheritance tax before any distributions to beneficiaries

Mistake #6:

Assuming Small Estates Don't Owe Tax

Problem:

Even $50,000 estates owe inheritance tax if transferred to children (4.5%)

Solution:

File return and pay tax regardless of estate size

PA Probate Help's Inheritance Tax Support

We Help Executors:

Estimate tax obligations early for planning purposes

Coordinate property sales to provide liquidity for tax payments

Calculate discount savings from quick property sales

Time property sales to capture 3-month discount

Obtain property appraisals for accurate tax valuations

Connect with estate CPAs specializing in PA inheritance tax

Provide documentation for tax return preparation

Verify tax payments made properly and timely

Navigate county Register of Wills filing procedures

We DON'T:

Prepare tax returns (hire CPA/attorney for this)

Provide tax advice (consult tax professional)

File tax documents (attorney/CPA service)

We DO:

Provide property expertise that supports tax planning

Help executors understand tax implications of property decisions

Coordinate property sales with tax deadlines

Connect executors with qualified tax professionals

Managing Property Tax Obligations on Inherited Real Estate

The Challenge:

Property taxes (real estate taxes) are separate from inheritance tax and create their own set of challenges for Pennsylvania executors. Unlike inheritance tax (one-time transfer tax), property taxes are annual obligations that continue regardless of death or probate status.

Understanding Pennsylvania Property Taxes

Who Levies Property Taxes:

Pennsylvania property taxes typically include THREE separate bills:

County taxes

School district taxes (usually the largest)

Municipal/Township taxes

Each taxing authority sends separate bills with different due dates, creating administrative complexity.

Why PA Property Taxes Are High:

Pennsylvania relies heavily on property taxes for school funding, resulting in some of the nation's highest rates:

Statewide average: 1.36% of home value annually

Montgomery County: Often 2.5-3.5% annually

Philadelphia: 1.0-1.3% (lower due to city services funded other ways)

Bucks County: 1.5-2.5% depending on township

Delaware County: 1.7-2.3% typically

Chester County: 1.5-2.2% varying by township

Example: Home valued at $300,000 in Montgomery County:

Annual property taxes: approximately $7,500-$10,500

Monthly equivalent: $625-$875

During 12-month probate, that's $7,500-$10,500 in

estate expenses just for property taxes on one house

Common Property Tax Scenarios Executors Face

Scenario 1:

Deceased Was Current on Taxes

Situation:

All property taxes paid up to date of death. New bills arrive during probate.

Executor Responsibility:

Pay taxes as bills arrive

Use estate checking account

Keep bills and payment records

Consider whether to pay from estate reserves or wait for property sale proceeds

Timeline Impact:

Typical 9-18 month probate = 1-2 property tax bills

Must factor into cash flow planning

Solution:

Budget for property taxes when estimating estate expenses. If estate lacks cash, may need to sell property quickly or borrow against estate assets.

Scenario 2:

Taxes Delinquent at Death

Situation:

Deceased fell behind on property taxes before death - sometimes multiple years of arrears.

Common Causes:

Financial hardship in final years

Cognitive decline (forgetting to pay)

Terminal illness (stopped caring about bills)

Overwhelming debt (prioritized other expenses)

What Executors Inherit:

Unpaid tax principal (often $5,000-$30,000+)

Penalties and interest (10-18% annually in PA)

Tax liens on the property

Potential sheriff's sale proceedings

Urgent Problem:

Cannot sell property with tax liens. Must be resolved before closing.

Solution Path:

Step 1:

Determine Exact Amount Owed

- Contact each taxing authority (county, school, township)

- Request "payoff statement" showing principal + penalties + interest

- Get breakdown by tax year

Step 2:

Verify Lien Status

- Check county records for recorded liens

- Determine if property on sheriff's sale list

- Understand timeframe before forced sale

Step 3:

Negotiate

Some PA taxing authorities will:

- Waive or reduce penalties (not always, but ask)

- Accept payment plan (some counties/townships)

- Accept payment at closing from sale proceeds (common)

Step 4:

Prioritize Payment

Pennsylvania law gives property taxes SUPER-PRIORITY over almost all other debts. They must be paid before:

- Credit card debts

- Personal loans

- Most other unsecured debts

- Even before distributions to beneficiaries

Step 5:

Pay from Estate Funds

Options

- Pay immediately from estate bank accounts if funds available

- Escrowed at closing (buyer's funds pay liens, remainder to estate)

- Short-term estate loan if necessary to prevent sheriff's sale

Scenario 3:

Taxes Accumulate During Long Probate

Situation:

Probate takes 18-24 months (common with will contests, complex estates). Multiple tax bills arrive.

The Math:

$8,000 annual property taxes over 2 years = $16,000 in carrying costs, plus:

Mortgage payments

Insurance

Utilities

Maintenance

Executor Dilemma:

Estate may not have cash for ongoing payments

Can't sell property immediately (legal restrictions)

Property deteriorates if utilities shut off

Risk of property going to sheriff's sale

Solution:

Maintain minimal necessary services

Negotiate payment arrangements with taxing authorities

Seek court permission for quick sale if property burden threatens estate

Consider rental income to offset costs (if property suitable)

Scenario 4:

Property Assessment Increase

Situation:

Property hasn't been reassessed in decades. Death/ownership transfer triggers reassessment. Taxes suddenly increase.

Example:

Property assessed at $150,000 (hasn't been reassessed since 1990)

Actual market value $300,000

New assessment triggers $5,000/year tax increase

Impact on Estate:

Higher ongoing costs during probate

Affects property sale net proceeds calculation

May trigger beneficiary complaints

Solution:.

Understand that reassessment is legal and expected

Factor new assessment into sale pricing

Consider appealing assessment if truly excessive (requires proof of overvaluation)

Plan for higher holding costs until sale

Pennsylvania Property Tax Relief Programs

Homestead Exemption:

Reduces assessed value for owner-occupied primary residences. Deceased may have been receiving this.

Executor Note:

Homestead exemption typically ends at death. Estate property loses this benefit, increasing tax burden during probate.

Senior Citizen Rebates:

Deceased may have been receiving Property Tax/Rent Rebate.

Executor Note:

Can file for prorated rebate for portion of year deceased was alive. Any rebate check received is estate asset.

Tax Abatement (Philadelphia):

10-year property tax abatement for new construction/major renovations.

Executor Note:

Abatement status transfers with property at sale. May affect value.

Impact of Property Taxes on Sale Strategy

Property taxes directly affect executor's decisions:

Quick Sale Benefits:

Example:

Stops ongoing tax obligations sooner

Reduces total estate carrying costs

Prevents tax arrears from accumulating

Avoids risk of sheriff's sale

Holding Property Considerations:

Calculate monthly tax burden

Determine if estate has resources to carry taxes

Consider whether holding period appreciation offsets tax costs

Factor in whether quick sale captures PA inheritance tax discount

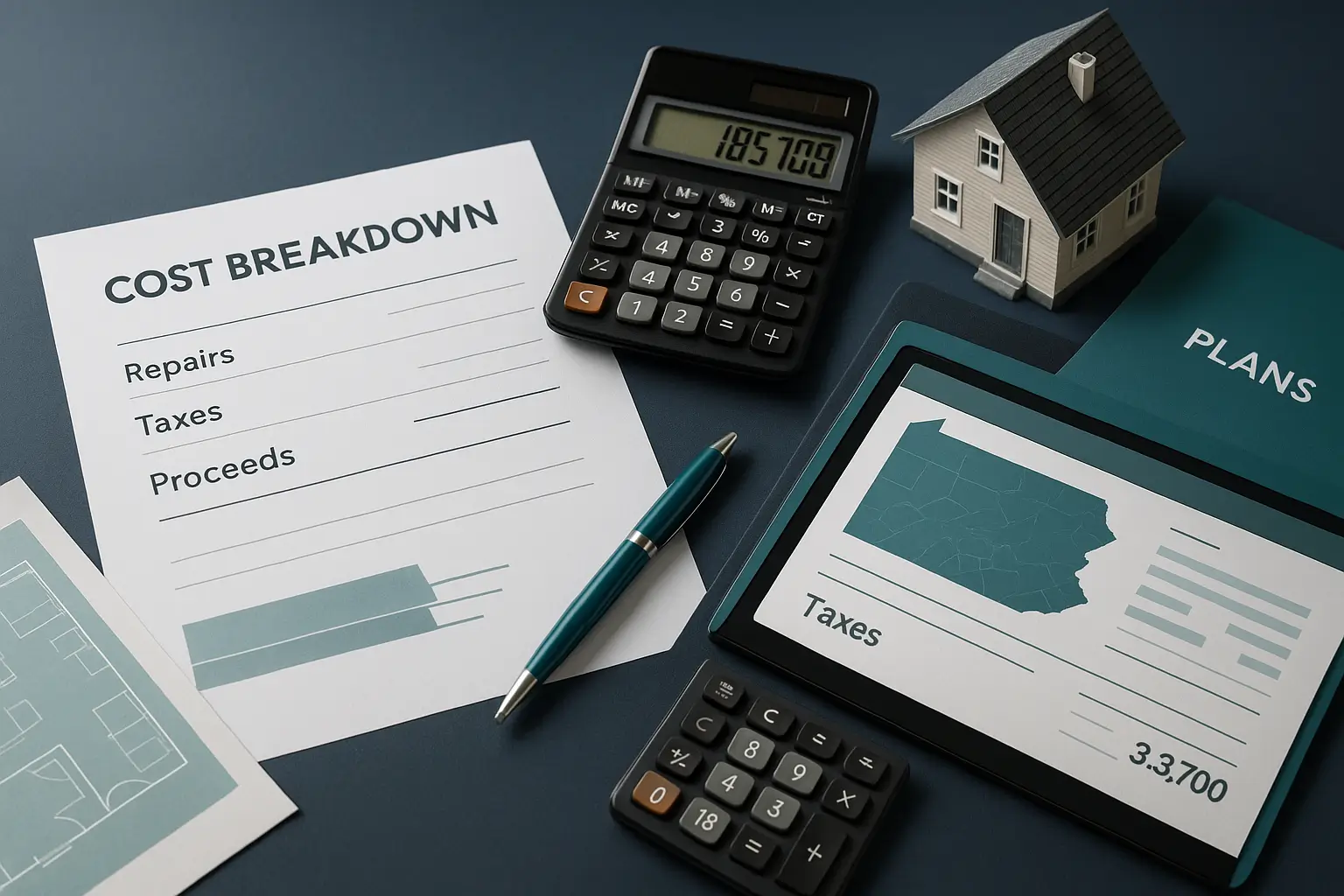

Example Analysis:

Option A: Invest 4 Months + $20,000 in Repairs

Sale price: $325,000

Less repair costs: -$20,000

Less 4 months property taxes: -$3,200

Less other carrying costs: -$4,000

Net: $297,800

Option B: Sell As-Is Immediately

Sale price: $295,000

Less repairs: $0

Less property taxes: $0 (immediate sale)

Less carrying costs: $0

Net: $295,000

In this scenario, delaying for repairs costs $2,800 despite $30,000 higher sale price.

PA Probate Help Analysis:

We run these calculations with actual property tax amounts, realistic repair costs, and current market data to help executors make informed decisions.

Property Tax Payment Logistics

During Probate:

Executor pays from estate checking account

Keep all receipts and canceled checks

Document in estate accounting

Don't use personal funds (you'll need to be reimbursed)

At Property Sale:

Title company handles prorated tax payments at closing

Buyer pays taxes from date of purchase forward

Estate responsible for taxes through closing date

Escrowed amounts for delinquent taxes paid from buyer's funds at closing

After Distribution:

If property distributed to beneficiary rather than sold:

Beneficiary assumes all future tax obligations

Executor should confirm taxes current before distribution

Beneficiary signs receipt acknowledging property condition including tax status

PA Probate Help's Property Tax Support

We Assist Executors With:

Research property tax status across all taxing authorities

Obtain payoff statements for delinquent taxes

Calculate total tax burden during probate timeline

Factor property taxes into sale strategy (hold vs. quick sale)

Coordinate with tax collectors for payment arrangements

Ensure proper tax handling at closing

Provide documentation for estate accounting

Connect with property tax appeal attorneys if needed

Critical Service:

We prevent executors from being blindsided by property tax issues that derail sales or drain estate resources.

Federal Estate Tax: Do You Need to Worry?

Short Answer for Most: NO

Federal estate tax only affects the wealthiest 0.1% of estates. If the deceased's total estate (everything they owned anywhere) is under $13.99 million (2025), you don't owe federal estate tax.

What Counts Toward Federal Estate Tax Exemption?

Everything Deceased Owned Worldwide:

Real estate (all locations)

Bank/investment accounts

Retirement accounts (IRAs, 401(k)s)

Business interests

Life insurance (if deceased owned policy)

Personal property

Assets transferred before death (in some cases)

Plus:

Gifts made in prior years (over annual exclusion)

Certain transfers to family (under specific rules)

Not Included:

Property left to spouse (unlimited marital deduction)

Property left to charity (charitable deduction)

Life insurance owned by others

When Federal Estate Tax Applies

Estates Under $13.99 Million:

No federal estate tax owed

Still must file Pennsylvania inheritance tax return

No federal Form 706 required (with exception below)

Estates Over $13.99 Million:

Federal estate tax owed on amount exceeding exemption

Must file Form 706 (federal estate tax return)

Requires sophisticated estate planning attorney + CPA

Complex valuations of all assets

Potential estate tax strategies

Exception - Portability Election:

Even if estate under exemption, surviving spouse may want to file Form 706 to elect "portability" - transferring unused exemption to surviving spouse for future use.

Pennsylvania Property and Federal Estate Tax

Real Estate Valuation Critical:

Pennsylvania estate property must be professionally appraised for federal estate tax purposes if Form 706 required.

Valuation Date Options:

Date of death value (most common)

Alternate valuation date (6 months after death) - can reduce tax if property values declined

Property Sales and Estate Tax:

If property sold before Form 706 filed:

Report date of death value on Form 706

Any gain/loss from sale reported separately on estate income tax return

Sale doesn't change estate tax calculation (based on date of death value)

After Distribution:

If property distributed to beneficiary rather than sold:

Beneficiary assumes all future tax obligations

Executor should confirm taxes current before distribution

Beneficiary signs receipt acknowledging property condition including tax status

PA Probate Help's Role with Federal Estate Tax

We DON'T:

Prepare Form 706 (requires estate tax attorney/CPA)

Provide tax advice on federal estate tax

Handle estate tax negotiations with IRS

We DO:

Help identify when estates may exceed exemption threshold

Coordinate property appraisals for federal estate tax purposes

Connect executors with estate tax attorneys and CPAs

Manage property sales timing with federal estate tax considerations

Provide documentation for estate tax return preparation

Critical Service:

If Your Estate May Exceed Federal Exemption:

You need sophisticated professional help immediately. PA Probate Help connects you with Pennsylvania estate tax attorneys and CPAs who specialize in high-net-worth estates.

Three Income Tax Returns May Be Required

Decedent's Final Individual

Income Tax Return

Covers:

January 1 through date of death

Includes:

Wages/salary earned before death

Investment income (interest, dividends, capital gains) before death

Rental income from property before death

Business income before death

All normal income tax items

Filed On:

Form 1040 (individual return)

Due Date:

April 15 of year following year of death (standard tax deadline)

Who Files:

Executor, signing as "executor/personal representative"

Property Relevance:

If deceased received rental income from property before death, must be reported on final return.

Estate Income Tax Return (if required)

Covers:

Date of death through estate termination

Estate Generates Income From:

Interest on estate bank accounts

Dividends from investment accounts

Rental income from estate property

Capital gains from sale of estate assets

Business income from estate-owned business

Any income earned by estate assets during administration

Filed On:

Form 1041 (estate/trust return)

Required If:

Estate gross income exceeds $600 per year

Due Date:

April 15 (annual) or quarterly estimated payments if income substantial

Property Relevance:

Rental income during probate creates estate taxable income

Property sale gains (over date of death value) create estate income

Property-generated income must be reported

Inheritance/Beneficiary Income Tax

When Beneficiaries Receive:

Assets from estate, they may have future income tax on:

Includes:

Income generated by inherited property after distribution

Capital gains if they later sell inherited property

Rental income if they keep rental property

"Step-Up in Basis" Rule:

Inherited property gets new "cost basis" = fair market value on date of death.

Example:

Deceased bought house in 1970 for $50,000

Worth $300,000 at death

Beneficiary inherits it

Beneficiary's basis = $300,000 (not $50,000)

If beneficiary sells for $310,000, only $10,000 capital gain (not $260,000)

This is HUGE tax benefit of inheritance.

Property Sales and Capital Gains

Scenario:

Estate sells property during probate

Everything Deceased Owned Worldwide:

Tax Analysis:

Date of Death Value:

$300,000 (per appraisal)

Sale Price:

$315,000

Result: $15,000 capital gain to estate

Estate owes income tax on $15,000 gain

(not beneficiaries, not inheritance tax - this is separate income tax on the gain).

Federal capital gains rate for estates:

15-20% depending on estate tax bracket

Pennsylvania:

No state capital gains tax (income taxed as regular income)

Strategies to Minimize:

Sell quickly - less time for appreciation = less gain

Deduct selling costs - realtor commission, repairs, closing costs reduce gain

Allocate to beneficiaries - sometimes estate can pass gain through to beneficiaries if distributed before sale

Professional tax planning - CPA can structure to minimize tax

When Federal Estate Tax Applies

If Estate Owns Rental Property:

During Probate:

Rental income = estate income

Must report on Form 1041

Must pay estimated taxes quarterly if income substantial

Can deduct expenses (maintenance, insurance, taxes, depreciation)

Executor Decisions:

Continue renting during probate (generates income but creates admin burden)

Evict tenants and sell vacant (cleaner but loses rental income)

Sell with tenants in place (common investor buyer strategy)

Tax Considerations:

Rental income helps offset property carrying costs

But creates estate tax complexity

Must file quarterly returns (administrative burden)

Depreciation recapture issues on sale

Property-Related Tax Deductions

Executors Can Deduct on Estate Returns:

Property maintenance costs during probate

Property management fees (if rental property)

Property insurance

Property taxes paid by estate

Mortgage interest on estate property

Repairs to maintain property value

Utilities for estate property

Realtor commissions on property sale

Legal fees related to property matters

Appraisal fees for property valuations

Cannot Deduct:

Capital improvements (added to property basis instead)

Personal expenses of executor

Expenses benefiting executor personally

Record-Keeping Critical:

Save all receipts, invoices, bills for property-related expenses. These reduce estate income tax and can be claimed on inheritance tax return as deductions.

PA Probate Help's Income Tax Support

We Help:

Track property income/expenses for tax reporting

Provide documentation to estate CPA/tax preparer

Coordinate property sales with tax year planning

Manage rental property during probate if continued

Calculate property gains/losses for tax purposes

Connect with estate tax professionals

Time property sales to minimize estate income tax

We Connect Executors With:

Estate CPAs who prepare Form 1041

Tax preparers familiar with Pennsylvania estates

Tax attorneys for complex situations

Enrolled agents for IRS issues

Pennsylvania Estate Property Tax Deadlines You Cannot Miss

Executors must juggle multiple tax deadlines simultaneously. Missing any deadline costs the estate money in penalties, interest, and lost opportunities.

MONTH 0:

(Death Occurs) Immediate Actions

- Obtain death certificates

- Secure estate property

- Stop automatic payments

- Begin asset inventory

Tax Impact:

"Tax clock" starts at date of death for all deadlines.

MONTH 1:

Initial Organization

- File will with Register of Wills

- Obtain Letters Testamentary

- Open estate bank account

- Apply for estate EIN (tax ID number)

Tax Impact:

Estate EIN required for estate bank accounts and future tax filings.

MONTH 2:

Asset Consolidation

- Inventory all estate assets

- Obtain property appraisals

- Value all accounts

- Identify debts

Tax Impact:

Values as of date of death determine inheritance tax. Get appraisals early.

MONTH 3:

CRITICAL DEADLINE Pennsylvania Inheritance Tax Prepayment

Inheritance Tax Prepayment Discount DEADLINE: 3 Months from Death

Action Required:

Pay estimated Pennsylvania inheritance tax to capture 5% discount.

Why Critical:

On $20,000 tax bill, missing this deadline costs estate $1,000.

Strategy:

- Estimate inheritance tax (conservative)

- Make payment by 3-month deadline

- File formal return later with exact numbers

- Get refund if overpaid (with discount)

Property Connection:

Selling estate property within 3 months provides liquidity for this payment. Quick property sales often justified SOLELY by capturing this discount.

MONTHS 3-6:

Property Management Period

- Property sales typically begin

- Continue paying property taxes

- Maintain insurance

- Handle ongoing property costs

Tax Impact:

Every month of property holding costs accumulate. Balance quick sale vs. maximizing price.

MONTH 6:

Mid-Point Assessment

- Review estate finances

- Assess progress toward final distribution

- File any required quarterly estate income tax estimates

Tax Impact:

If estate generating income (rental property, investments), first quarterly Form 1041 estimated payment may be due.

MONTH 9:

CRITICAL DEADLINE Pennsylvania Inheritance Tax Return DUE

DEADLINE: 9 Months from Death

Action Required:

File complete PA Inheritance Tax Return (Form REV-1500) with county Register of Wills.

Complete asset inventory and values

List of all beneficiaries and relationships

Deductions claimed (debts, funeral, admin costs)

Tax calculation

FULL PAYMENT (if not already paid)

What's Filed:

Penalty for Late Filing:

- Interest charges (approximately 6%

annually)

- Penalties for substantial underpayment

- PA Department of Revenue collection actions

Property Connection:

Most estates sell property by this deadline to have funds available for tax payment.

MONTH 9:

ALSO 🇺🇸 Federal Estate Tax Return (if applicable)

DEADLINE: 9 Months from Death

Required Only If:

Estate exceeds $13.99 million (2025 exemption)

Form:

706 (complex, requires attorney/CPA)

Extension Available:

6-month extension possible, but payment still due at 9 months.

MONTH 9: also US Federal Estate Tax Return (if applicable)

DEADLINE: 9 Months from Death

Required Only If:

Estate exceeds $13.99 million (2025 exemption)

Form: 706 (complex, requires attorney/CPA)

Extension Available:

6-month extension possible, but payment still due at 9 months.

APRIL 15 (Year Following Death) Decedent's Final Income Tax Return

DEADLINE: April 15 of year following year of death

Form: 1040 (individual return)

Covers: January 1 through date of death

Executor Signs: As personal representative

Extension Available:

Standard 6-month extension to October 15 (file Form 4868)

Property Relevance:

If deceased received rental income or sold property before death, must be reported.

ONGOING (Throughout Administration) Estate Income Tax Returns

Form 1041 - Filed Annually (or Quarterly Estimated)

Due: April 15 annually (for prior calendar year)

Required If:

Estate gross income exceeds $600 per year

Common Sources:

- Interest on estate bank accounts

- Rental income from estate property

- Capital gains from asset sales

- Investment income

Property Connection:

Selling estate property often generates capital gains requiring Form 1041 filing.

Property Tax Bills (Varies by Location) Ongoing Obligation

Pennsylvania Property Tax Timing:

- School taxes: Summer/Fall typically

- County taxes: Various schedules

- Municipal taxes: Various schedules

Executor Responsibility:

Pay all property tax bills as they arrive from estate funds until property sold or distributed.

No Deadline Flexibility:

Property taxes become delinquent per local schedule (30-90 days after bill date typically). Liens filed quickly thereafter.

PA Probate Help's Deadline Management:

We help executors:

Track all tax deadlines from date of death

Coordinate property sales with critical 3-month and 9-month deadlines

Calculate whether quick sale justifies capturing discount

Provide reminders and deadline alerts

Connect with tax professionals for filing

Ensure property taxes paid timely during probate

SUMMARY OF CRITICAL DEADLINES:

Deadline

3 Months

9 Months

9 Months

April 15

April 15

Ongoing

Tax Type

PA Inheritance Tax Prepayment

PA Inheritance Tax Return

Federal Estate Tax (if applicable)

Final Individual Income Tax

Estate Income Tax (annual)

Property Taxes

Consequence of Missing

Lose 5% discount (often $1,000-$10,000+)

Interest + penalties (~6% annually)

Interest + penalties (substantial)

Interest + penalties (standard IRS)

Interest + penalties

Liens, sheriff's sale, forced liquidation

Estate Tax Professional Network

Estate tax complexity requires specialized professionals. PA Probate Help connects executors with Pennsylvania tax experts who understand probate situations.

Estate CPAs

Services:

Pennsylvania inheritance tax return preparation

Estate income tax returns (Form 1041)

Final individual income tax returns

Tax planning and strategy

Audit support if needed

When You Need:

All PA estates (inheritance tax return)

Estates generating income

Complex asset situations

High-value estates

PA Probate Help Connection:

We refer to CPAs specifically experienced with Pennsylvania estate taxation and probate property issues.

Estate Tax Attorneys

Services:

Federal estate tax planning

Complex PA inheritance tax issues

Tax appeals and disputes

Estate tax litigation

Advanced tax strategies

What You Need:

Estates over $13.99M (federal estate tax)

PA inheritance tax disputes

Complex business valuations

Will contests affecting taxation

IRS or PA Dept Revenue audits

PA Probate Help Connection: Network includes top Pennsylvania estate tax attorneys in all five counties we serve.

Enrolled Agents

Services:

IRS representation

Tax resolution

Estate income tax preparation

Tax planning

Audit representation

What You Need:

IRS issues or questions

Complex estate income tax

Federal tax problems

Cost-effective tax prep alternative

PA Probate Help Connection: Enrolled agents specializing in estate and trust taxation.

Property Tax Specialists

Services:

Property tax appeals

Assessment challenges

Tax lien resolution

Payment plan negotiation

Municipal tax issues

What You Need:

Property over-assessed

Delinquent property tax issues

Tax liens on estate property

Assessment increase disputes

PA Probate Help Connection:

Local specialists in each Pennsylvania county we serve.

Government Resources

Pennsylvania Department of Revenue

Inheritance Tax Division

Website: revenue.pa.gov

Phone: (717) 787-8327

Inheritance tax forms and publications

County Register of Wills Offices

Montgomery: (610) 278-3340

Philadelphia: (215) 686-6250

Bucks: (215) 348-6265

Delaware: (610) 891-4355

Chester: (610) 344-6335

IRS Estate & Trust Information

Estate tax information

Form 706 instructions

Form 1041 instructions

Website: irs.gov/businesses/small-businesses-self-employed/estate-and-gift-taxes

Property Tax Strategy: Maximizing Estate Value

Minimize total tax burden on estate while fulfilling all legal obligations and maximizing distributions to beneficiaries.

Strategic Principle #1:

Speed Often Saves Money

The 3-Month Window:

Pennsylvania's 5% inheritance tax discount creates powerful incentive for quick action.

Property Sale Math:

Scenario:

Estate with $400,000 house, inherited by 2 children

Inheritance Tax:

$400,000 × 4.5% = $18,000

Pay within 3 months discount (5% of $18,000) = $900 savings

Quick Sale vs. Waiting:

Option A:

Sell within 3 months

Accept offer: $385,000 (slightly below market for quick sale)

Capture discount: -$900 inheritance tax saved

3 months carrying costs: -$4,500

Net value: $380,400 ($385,000 - $4,500)

Option B:

Wait 6 months for better price

Higher offer: $400,000 (full market value)

Miss discount: Pay full $18,000 tax (no discount)

6 months carrying costs: -$9,000

Net value: $391,000 ($400,000 - $9,000)

The Point:

Run actual numbers for your situation. Sometimes quick sales justified by discount alone.

Strategic Principle #2:

Document Everything

Tax Deductions Require Proof:

Track all property-related expenses:

Property tax payments (bills + canceled checks)

Insurance payments (policies + proof of payment)

Utility bills paid by estate

Maintenance and repair invoices

Lawn care / snow removal receipts

Realtor commission (closing statement)

Appraisal fees (invoice)

Legal fees for property matters (itemized bills)

Mortgage interest paid (statements)

Why documentation matters:

Reduces inheritance tax (deductible administration expenses)

Reduces estate income tax (deductible operating expenses)

Protects executor from beneficiary challenges

Proves proper estate management

Required for tax audits

PA Probate Help Service:

We help executors establish organized filing systems for property expenses and provide summary reports for tax preparers.

Strategic Principle #3:

Coordinate Property and Tax Timing

Property sales affect multiple tax obligations:

Sell in Year 1 (Year of Death):

Capital gain (if any) reported on estate income tax for year 1

Proceeds available for inheritance tax payment

May capture 3-month discount

Sell in Year 2:

Capital gain reported on year 2 estate income tax

Extends estate administration (more carrying costs)

Misses 3-month discount

But may allow higher price if market improving

Tax Year Planning:

If selling in December vs. January affects tax year, consider:

Estate income tax rates and brackets

Timing of estate termination

Capital gains implications

Overall tax strategy

Professional Coordination:

PA Probate Help works with estate CPAs to time property sales advantageously for tax purposes.

Strategic Principle #4:

Consider Property Condition and Tax Trade-Offs

To Repair or Not to Repair - Tax Perspective:

Repairs Made by Estate:

Immediately deductible on estate income tax return (reduces estate income tax)

Also deductible on PA inheritance tax return (reduces inheritance tax)

Both deductions = significant tax benefit

But requires estate cash outlay upfront

No Repairs (As-Is Sale):

No cash outlay

No deductions

But faster sale (potentially captures discount)

Lower carrying costs

Tax-Optimized Decision:

Sometimes modest repairs justified because tax deductions make net cost lower than it appears.

Example:

$10,000 in repairs:

Deduct from PA inheritance tax = saves ~$450 (4.5% of $10,000)

Deduct from estate income tax = saves ~$2,000-$3,000 (20-30% rate)

Net cost of repairs: ~$6,500-$7,500 (after tax savings)

If repairs increase sale price by $15,000, you net $7,500-$8,500 gain after tax benefits.

Strategic Principle #5:

Use Professional Expertise

DIY Estate Tax = Expensive Mistakes:

Common costly errors:

Missing 3-month inheritance tax discount ($1,000-$10,000+ lost)

Incorrect property valuations (PA Dept Revenue audits and assesses additional tax)

Failing to claim all deductions (overpaying tax)

Missing property tax deadlines (liens, penalties, sheriff's sales)

Improper property sale timing (unnecessary capital gains tax)

Not coordinating multiple tax returns (duplication or omissions)

Professional Investment Returns Multiples:

Hiring estate CPA costs: $2,000-$5,000 typically

Value provided: $5,000-$25,000+ in tax savings

ROI: 200-500%

PA Probate Help saves money by:

Providing property expertise that supports tax planning

Connecting with right tax professionals

Coordinating property sales with tax deadlines

Managing property costs (reducing taxable estate)

Ensuring documentation for tax deductions

Strategic Principle #6:

Communicate with Beneficiaries About Taxes

Beneficiaries Need to Understand:

Taxes significantly reduce estate value (often 10-20% of gross estate)

Inheritance tax must be paid before distributions

Property carrying costs reduce inheritances monthly

Quick property sales may be necessary for tax purposes

Lower sale prices sometimes result in higher net proceeds (discount capture)

Transparency Prevents Conflicts:

When beneficiaries understand tax obligations and strategy, they're more likely to:

Support quick property sales

Accept as-is sale decisions

Not question executor's judgment

Understand final distribution amounts

PA Probate Help Communication Support:

We provide beneficiary-friendly explanations of tax implications and property decisions, helping executors maintain family harmony.

Frequently Asked Questions About Estate Property Taxes

Do I have to pay Pennsylvania inheritance tax if the estate is small?

Yes, Pennsylvania inheritance tax applies to estates of any size if property is transferred to taxable beneficiaries.

There's no minimum estate value exemption. Even a $50,000 estate transferred to children owes $2,250 in inheritance tax (4.5% of $50,000).

The only way to avoid PA inheritance tax is if all property passes to: spouse (0% tax), charities (0% tax), or a parent from a child under 21 (0% tax).

Small estates may qualify for simplified probate procedures, but inheritance tax still applies based on who receives the property.

Many executors mistakenly believe small estates don't owe inheritance tax - this is incorrect and can result in late filing penalties.

PA Probate Help helps executors of all estate sizes understand and fulfill inheritance tax obligations, regardless of estate value. File the return and pay the tax even for modest estates.

Can I deduct funeral expenses and debts from Pennsylvania inheritance tax?

Yes, Pennsylvania allows specific deductions that reduce the taxable estate value before calculating inheritance tax.

Allowable deductions include: funeral and burial expenses (reasonable amounts, typically $10,000-15,000 accepted without question), debts owed by deceased at death (credit cards, personal loans, medical bills with documentation), mortgages and liens on property, estate administration expenses (attorney fees, executor compensation, court costs, appraisal fees, accounting fees), and federal estate tax if applicable (rare).

Cannot deduct: gifts made before death, property passing to spouse (already 0% tax), normal living expenses, estimated future expenses.

How it works: Start with gross estate value (all assets), subtract allowable deductions, apply tax rates to net amount distributed to each beneficiary based on their relationship. Proper documentation critical - PA Department of Revenue may challenge excessive deductions. Save all receipts, invoices, and bills.

PA Probate Help coordinates with estate CPAs to ensure all allowable deductions are claimed, potentially saving thousands in inheritance tax.

What happens if I miss the 3-month Pennsylvania inheritance tax discount deadline?

You lose the 5% discount permanently—there's no way to capture it after the 3-month deadline passes.

Financial impact: On $20,000 inheritance tax, missing the deadline costs the estate $1,000. On $50,000 tax, you lose $2,500. On $100,000 tax, you forfeit $5,000. This is real money directly reducing beneficiary inheritances.

The deadline is strict: Exactly 3 calendar months from date of death. Payment must be received by Register of Wills by this date (postmark doesn't count—they must have payment in hand). Strategy to avoid missing it: Make estimated payment within 3 months even if you don't have exact numbers.

Pennsylvania allows you to pay estimated amount early, then file formal return with final calculations later. If you overpaid, you get refund with the 5% discount applied. If you underpaid, you pay balance but still got discount on the early payment. This is why quick property sales matter: Selling estate real estate within 3 months provides cash to capture this substantial discount.

PA Probate Help often recommends accepting slightly lower offers on quick sales because the inheritance tax discount savings offset the lower price.

Do beneficiaries pay inheritance tax or does the estate pay it?

Technically, Pennsylvania inheritance tax is the responsibility of the beneficiary receiving the property - the tax is on their "right to receive" the inheritance.

However, in practice, the executor typically pays the entire inheritance tax from estate funds before distributing anything to beneficiaries. This is the standard approach because: it's simpler administratively (one payment to Register of Wills rather than tracking multiple beneficiary payments), ensures tax gets paid (executor control), prevents beneficiaries from receiving inheritance then failing to pay their share, and is required before estate can be closed and executor discharged.

How it's calculated: Each beneficiary's inheritance is taxed at their applicable rate (0%, 4.5%, 12%, or 15% based on relationship to deceased). The sum of all individual taxes = total estate inheritance tax. After estate pays: Beneficiaries receive net inheritances (after all taxes and expenses paid).

Exception: If estate lacks liquidity and property is distributed "in kind" to beneficiaries, they may be responsible for paying their share of inheritance tax on that property.

PA Probate Help helps executors understand tax payment logistics and ensures proper handling.

How do property sales affect Pennsylvania inheritance tax?

Property sales don't change the inheritance tax owed—inheritance tax is calculated on property value at date of death, regardless of whether property is later sold or distributed to beneficiaries.

Example: House worth $300,000 at date of death, later sold for $280,000 (market declined) or $320,000 (market improved). Inheritance tax is calculated on $300,000 regardless of actual sale price.

However, property sales affect inheritance tax in these ways:

(1) Timing for discount: Selling property within 3 months provides cash to capture 5% early payment discount.

(2) Liquidity: Sale proceeds provide funds to pay inheritance tax (otherwise estate may lack cash).

(3) Estate expenses: Longer property holding = higher carrying costs (property taxes, insurance, maintenance) = fewer estate assets available = less to beneficiaries after taxes.

(4) Separate income tax: If property sells for MORE than date of death value, the gain is subject to estate income tax (separate from inheritance tax).

Strategic consideration: Quick property sales often justified primarily to capture the 3-month inheritance tax discount, even if sale price is slightly lower than waiting would achieve.

PA Probate Help analyzes whether discount savings offset lower quick-sale price.

What if the estate doesn't have enough cash to pay Pennsylvania inheritance tax?

This is a common problem, especially when estate consists primarily of real estate with little liquid assets.

Solutions:

(1) Sell estate property quickly to generate cash for tax payment—most common approach.

(2) Borrow against estate assets (estate loan or line of credit) to pay taxes while waiting for better property sale timing.

(3) Beneficiaries loan money to estate for tax payment, reimbursed when property sells—requires written loan agreements.

(4) Request extension from PA Dept of Revenue for filing (6 months available) but payment still due at 9 months and interest charges continue—doesn't really solve cash problem.

(5) Payment plan negotiation with PA Dept of Revenue - sometimes available for hardship situations, requires formal application.

What NOT to do: Don't ignore the tax. PA Department of Revenue has collection powers including liens on estate property, garnishment of estate accounts, and personal liability for executor. Property sales are usually the answer: Even if market timing isn't ideal, generating cash to pay inheritance tax (especially within 3 months for discount) usually makes financial sense.

PA Probate Help specializes in quick estate property sales when tax payment creates urgency.

Are there any Pennsylvania property tax relief programs for inherited property?

Very limited relief specifically for inherited property. Homestead exemption (reduces assessed value for owner-occupied primary residence) typically ends at death - estate property no longer qualifies because it's not owner-occupied.

Senior citizen rebates deceased may have been receiving end at death (though you can file for prorated rebate for portion of year they were alive). Act 50/Clean and Green (farmland/open space preferential assessment) may transfer to beneficiaries if they continue qualifying use, but estate loses benefits if property sold. No special "probate property" tax breaks: Estate property pays full property taxes during administration.

Available relief programs:

Some Pennsylvania counties/municipalities offer:

property tax payment plans for delinquent taxes (not forgiveness, just spreading payment), hardship deferral programs (rare, usually requires occupancy), assessment appeals if property over-assessed (must prove actual market value lower than assessment).

Best approach: Pay property taxes timely to avoid delinquency penalties and liens. If estate truly cannot pay, contact taxing authorities immediately to explore options - waiting makes situation worse.

PA Probate Help connects executors with property tax specialists who negotiate payment arrangements when necessary.

How does jointly-owned property with rights of survivorship affect inheritance tax?

Jointly-owned property with rights of survivorship passes directly to surviving owner outside of probate, but Pennsylvania still assesses inheritance tax on deceased's interest in the property.

How PA treats joint ownership: Deceased's "contribution" to property is subject to inheritance tax based on surviving owner's relationship to deceased. Pennsylvania presumes 50/50 ownership unless you prove different contributions.

Examples:

(1) Spouses: House owned jointly by husband and wife → wife inherits husband's 50% → 0% inheritance tax (spouse exemption).

(2) Parent and child: Parent and adult child own house jointly → child inherits parent's 50% → 4.5% tax on parent's 50% of value.

(3) Siblings: Two sisters own house jointly → surviving sister inherits → 12% tax on deceased sister's 50%.

Joint bank accounts: Same rules - deceased's contribution (often presumed 50%) taxed based on survivor's relationship.

Right of survivorship means: Property passes automatically to survivor without probate, BUT doesn't avoid Pennsylvania inheritance tax.

Exception: Property owned jointly with spouse = 0% tax, effectively avoiding inheritance tax.

PA Probate Help helps executors understand joint property taxation and ensures proper reporting on inheritance tax returns.

What's the difference between Pennsylvania inheritance tax and federal estate tax?

Pennsylvania Inheritance Tax: State tax on the privilege of receiving property based on beneficiary's relationship to deceased. Tax rates: 0%-15% depending on relationship (spouse 0%, children 4.5%, siblings 12%, others 15%).

Applies to ALL estates regardless of size if property passes to taxable beneficiaries. Due 9 months from death. 5% discount for payment within 3 months. Filed with county Register of Wills. Federal Estate Tax: Federal tax on total value of deceased's estate if it exceeds exemption amount ($13.99 million in 2025). Tax rate: 40% on amounts over exemption. Only ~0.1% of estates pay federal estate tax. Due 9 months from death. No discount for early payment. Filed with IRS (Form 706).

Key differences: PA inheritance tax affects nearly all estates; federal estate tax affects only very wealthy estates. PA inheritance tax based on who receives property; federal estate tax based on total estate value.

You can owe Pennsylvania inheritance tax but not federal estate tax (common). You can theoretically owe federal estate tax but not PA inheritance tax (if everything to spouse/charity). Most Pennsylvania estates: Pay inheritance tax only, no federal estate tax.

PA Probate Help focuses primarily on inheritance tax and property tax issues affecting typical Pennsylvania estates.

Can property tax liens prevent me from selling estate property?

Yes, absolutely. Property tax liens must be resolved before property can be sold - title companies won't close with liens outstanding.

How property tax liens work: When property taxes become delinquent (typically 30-90 days after due date), taxing authority (county, school district, municipality) files lien against property. Lien attaches to property title and follows property through ownership changes. Creates legal claim against property for amount owed.

Impact on estate property sales: Buyer's title insurance won't be issued with liens present. Mortgage lenders won't fund loans on properties with liens. Prevents clean title transfer. Solution - liens paid at closing:

Most common approach: Property sold, title company pays off liens from sale proceeds at closing. Remaining proceeds after lien payoff go to estate.

Example: Property sells for $250,000. Property tax liens total $18,000. At closing: $18,000 paid to taxing authorities to satisfy liens, $232,000 (less closing costs) to estate.

Executor responsibility: Research all property tax liens before listing property. Obtain payoff statements showing exact amounts. Disclose liens to buyers upfront. Coordinate with title company for lien payoff at closing.

Avoid sheriff's sales: If delinquent taxes remain unpaid too long, property can be sold at sheriff's sale (forced liquidation) - usually for far less than market value.

PA Probate Help researches all property tax liens, obtains payoffs, and ensures proper resolution at closing. We prevent liens from derailing estate property sales.

Joe Thomas

Certified Probate Real Estate Specialist

If you have any questions about the probate process or would like to speak with a Certified Professional Real Estate professional about your specific probate needs, please use the following form to get in touch. We can also be reached directly at (215) 452-9415.

Contact Joe Thomas